1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

139

140

141

142

143

144

145

146

147

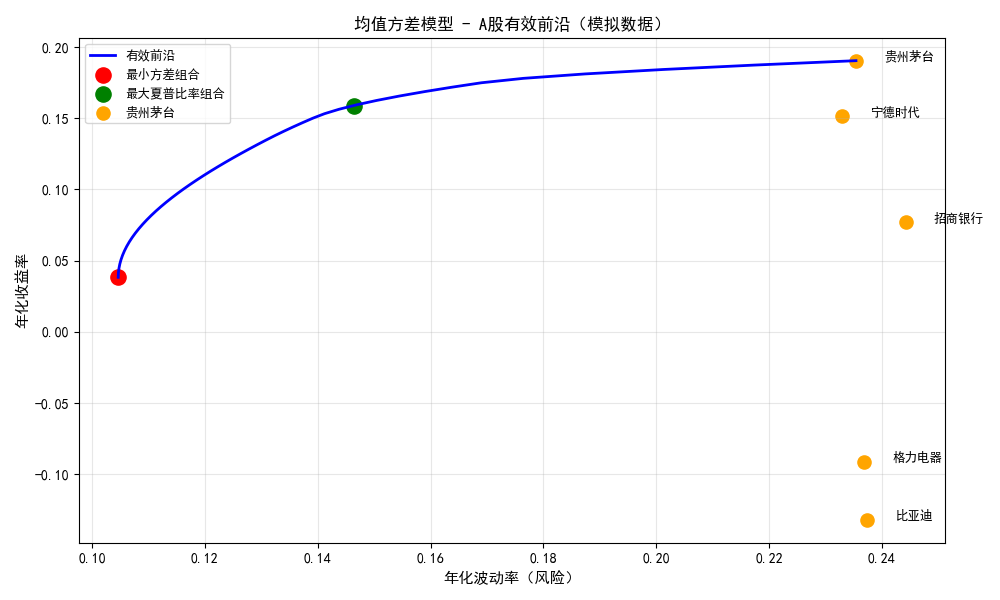

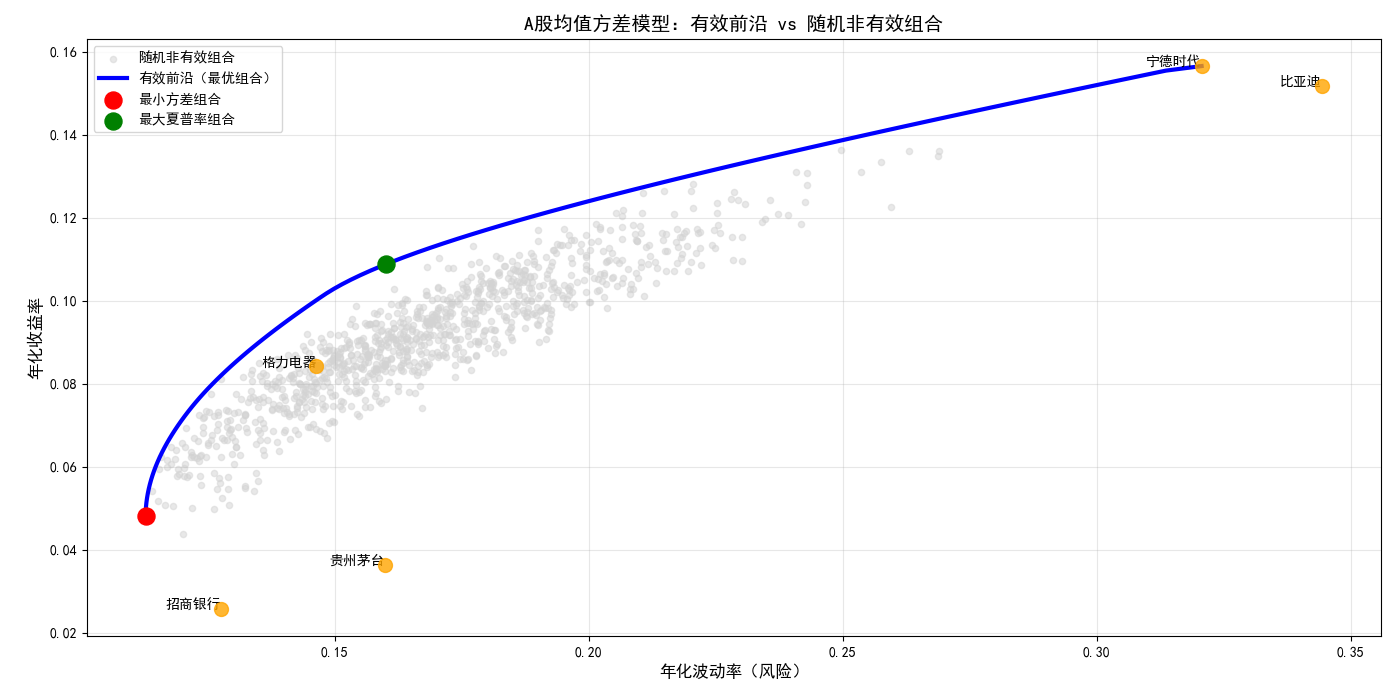

| 代码如下:

import pandas as pd

import numpy as np

import scipy.optimize as sco

import matplotlib.pyplot as plt

np.random.seed(42)

tickers = ['600519.SH', '300750.SZ', '600036.SH', '002594.SZ', '000651.SZ']

ticker_names = ['贵州茅台', '宁德时代', '招商银行', '比亚迪', '格力电器']

name_map = dict(zip(tickers, ticker_names))

n_days = 252 * 5

base_prices = [1000, 200, 30, 150, 30]

prices_data = []

for i in range(len(tickers)):

daily_ret = np.random.normal(0.0003, 0.015, n_days)

cum_ret = np.cumprod(1 + daily_ret)

price_series = base_prices[i] * cum_ret

prices_data.append(price_series)

prices = pd.DataFrame(

np.array(prices_data).T,

columns=tickers,

index=pd.date_range(start='2019-01-01', periods=n_days, freq='B')

)

daily_returns = np.log(prices / prices.shift(1)).dropna()

mu = daily_returns.mean() * 252

cov = daily_returns.cov() * 252

risk_free_rate = 0.02

def portfolio_performance(weights, mu, cov):

port_return = np.sum(mu * weights)

port_vol = np.sqrt(np.dot(weights.T, np.dot(cov, weights)))

sharpe_ratio = (port_return - risk_free_rate) / port_vol

return port_return, port_vol, sharpe_ratio

def minimize_volatility(weights, mu, cov):

return portfolio_performance(weights, mu, cov)[1]

def maximize_sharpe(weights, mu, cov):

return -portfolio_performance(weights, mu, cov)[2]

constraints = ({'type': 'eq', 'fun': lambda x: np.sum(x) - 1})

bounds = tuple((0, 1) for _ in range(len(tickers)))

initial_guess = np.array([1/len(tickers)] * len(tickers))

min_vol_result = sco.minimize(

minimize_volatility, initial_guess,

args=(mu, cov), method='SLSQP',

bounds=bounds, constraints=constraints

)

min_vol_weights = min_vol_result['x']

min_vol_return, min_vol_vol, _ = portfolio_performance(min_vol_weights, mu, cov)

max_sharpe_result = sco.minimize(

maximize_sharpe, initial_guess,

args=(mu, cov), method='SLSQP',

bounds=bounds, constraints=constraints

)

max_sharpe_weights = max_sharpe_result['x']

max_sharpe_return, max_sharpe_vol, _ = portfolio_performance(max_sharpe_weights, mu, cov)

target_returns = np.linspace(min_vol_return, mu.max(), 50)

target_vols = []

for target_ret in target_returns:

constraints_target = (

{'type': 'eq', 'fun': lambda x: np.sum(x) - 1},

{'type': 'eq', 'fun': lambda x: portfolio_performance(x, mu, cov)[0] - target_ret}

)

result = sco.minimize(

minimize_volatility, initial_guess,

args=(mu, cov), method='SLSQP',

bounds=bounds, constraints=constraints_target

)

target_vols.append(result['fun'])

target_vols = np.array(target_vols)

plt.rcParams['font.sans-serif'] = ['SimHei']

plt.rcParams['axes.unicode_minus'] = False

plt.figure(figsize=(10, 6))

plt.plot(target_vols, target_returns, 'b-', linewidth=2, label='有效前沿')

plt.scatter(min_vol_vol, min_vol_return, c='red', s=120, label='最小方差组合')

plt.scatter(max_sharpe_vol, max_sharpe_return, c='green', s=120, label='最大夏普比率组合')

for i, ticker in enumerate(tickers):

asset_vol = np.sqrt(cov.iloc[i, i])

asset_ret = mu[i]

plt.scatter(asset_vol, asset_ret, c='orange', s=90, label=ticker_names[i] if i==0 else "")

plt.text(asset_vol + 0.005, asset_ret, ticker_names[i], fontsize=9)

plt.xlabel('年化波动率(风险)', fontsize=11)

plt.ylabel('年化收益率', fontsize=11)

plt.title('均值方差模型 - A股有效前沿(模拟数据)', fontsize=12)

plt.legend(loc='upper left', fontsize=9)

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print("="*40)

print("均值方差模型计算结果(A股模拟数据)")

print("="*40)

print("\n【最小方差组合】(风险最低)")

print("-"*30)

for ticker, weight in zip(tickers, min_vol_weights):

print(f"{name_map[ticker]} ({ticker}): {weight:.2%}")

print(f"组合年化收益:{min_vol_return:.2%}")

print(f"组合年化波动率:{min_vol_vol:.2%}")

print("\n【最大夏普比率组合】(风险调整收益最高)")

print("-"*30)

for ticker, weight in zip(tickers, max_sharpe_weights):

print(f"{name_map[ticker]} ({ticker}): {weight:.2%}")

print(f"组合年化收益:{max_sharpe_return:.2%}")

print(f"组合年化波动率:{max_sharpe_vol:.2%}")

print(f"组合夏普比率:{(max_sharpe_return - risk_free_rate)/max_sharpe_vol:.2f}")

|